The “Johnson Guidelines” for Executor Commissions

Disclaimer: This content does not constitute legal advice. You should not act, or refrain from acting, based on the information provided without getting specific advice from your lawyer.

Some states provide an official statutory schedule outlining the maximum Executor fees based on the type and amount of estate assets. Unfortunately, for the Executor (or Administrator, in the case of an estate for someone who died without a Will) of a Pennsylvania estate, there is no such schedule issued by the state legislature. Instead, Pennsylvania statutory law simply says that the commission must be “reasonable and just under the circumstances.” An Executor who finds out they are entitled to a commission for their work may be left wondering how exactly they are supposed to know how much is reasonable and just?

Luckily, in the 1983 case In re: Johnson’s Estate, Judge Wood referenced a series of tables that can be used to calculate commissions and fees for simple estates based on the size and type of assets in the estate. While by no means the end of the question, this gives Executors some idea of how to go about determining the commission.

These guidelines, while they can serve as a general rule of thumb as to whether an amount is “reasonable and just” for a commission under Pennsylvania law, are not necessarily in-line with what a reasonable commission is for a particular estate. Other factors to be considered were set forth in another case, La Rocca Estate. For example, a larger commission may be warranted in a complex estate, such as one involving ongoing estate-related litigation or particularly complex assets and/or distributions.

That said, the so-called “Johnson Guidelines” can be cited as precedent and often support an Executor’s position if a commission were to be challenged that is at or below the amount calculated based on the Guidelines.

What are the Johnson Guidelines?

In the In re Johnson’s case, the Judge referenced a series of tables which, if followed, indicated that the commission was reasonable and just. Since this case, Pennsylvania Executors have often looked to these tables to calculate their commission. To determine the commission, an Executor needs to categorize the type of assets, determine the total value for each asset type, and apply the percentage to the asset category totals to arrive at the total commission.

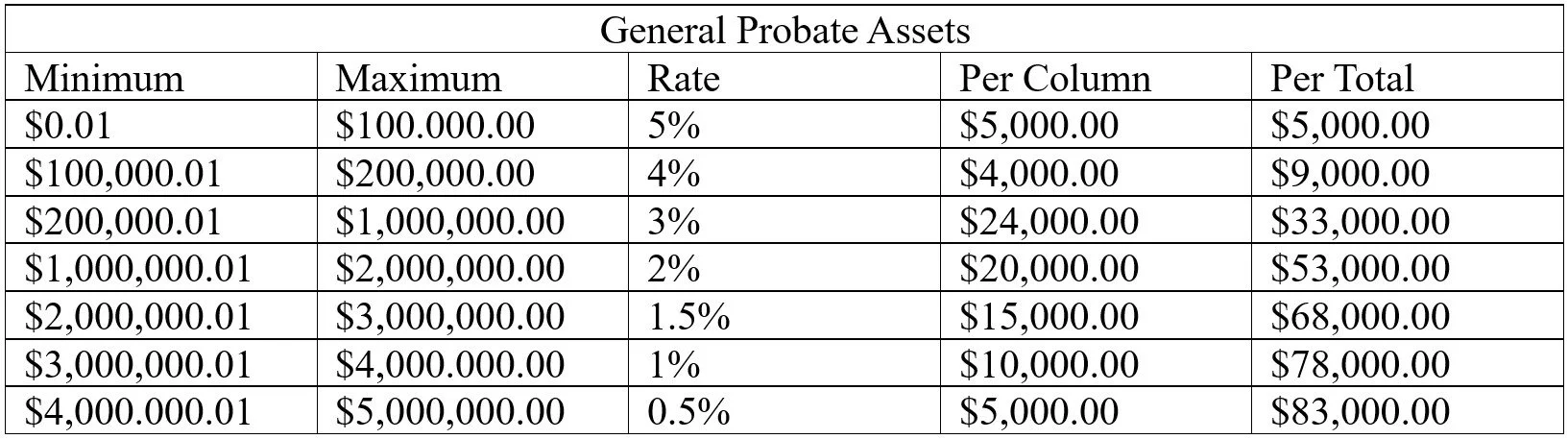

For general probate assets the calculation is comprised of a series of brackets, each with a descending rate of commission for the increasing amount of general probate assets. The table for general probate assets is as follows:

Other asset categories have their own percentages that apply. For example, for joint accounts, the commission is calculated at 1%, rather than the graduated table for general probate assets.

The other rates included in the Johnson Guidelines are as follows:

Joint Accounts – 1%

Real Estate Converted with the Aid of Broker – 3%

P.O.D. Bonds – 1%

Real Estate: Non-Converted – 5%

Trust Funds – 1%

Real Estate: Specific Devise – 1%

Example 1: Estate with $50,000 in general probate assets

For an estate containing $50,000 in probate assets, the Executor would apply the rate from the “General Probate Assets” table to the asset total. For probate assets more than $0.01 but less than $100,000, the rate is 5%. The Executor’s commission would be $50,000 x 5% = $2,500. An amount less than or equal to $2,500 would likely be reasonable under Pennsylvania law.

Example 2: Estate with $150,000 in general probate assets

If an estate’s probate assets are at the top of a range in the Johnson Guidelines, the number in the right-hand column shows the “running total” up to that maximum rate. For example, in an estate with $150,000 in probate assets, the table shows that for the first $100,000, the 5% rate applies. For the remaining $50,000, the 4% rate instead is used. The right-hand column for the 5% rate range shows the total amount in that bracket as 5,000 (that is, 5% of $100,000). The remaining $50,000 should be multiplied by 4% to arrive at $2,250. Thus, the total commission would be $7,250 ($5,000 plus $2,250).

Example 3: Estate with $1.5 million in general probate assets

The same analysis continues to apply for higher brackets. If an estate has $1.5M in probate assets, we can look to the last bracket for which the maximum range was reached. In this case, we are above the $1M bracket, but below the $2M maximum. Looking to the right-hand column for the bracket from $200,000.01 to $1M we can see that an estate with probate assets of exactly $1M would be eligible for $33,000 in commission based on those asset values. Amounts above $1M but less than $2M would be calculated based on the 2% rate for this range. In this estate, $500,000 x 2% = $10,000. This, plus the $33,000 allowable for probate assets up to $1M means the commission would be $43,000.

Example 4: Example 1 plus a joint account

“General probate assets” is not the only category that is used in determining commission. Other assets can be included in determining the commission amount and are based on a set percentage of the asset value, rather than a graduated scale like what is used for general probate assets.

For example, in an estate where the assets include Example 1’s $50,000 in probate assets and a joint account, we would need to look at a different portion of the Johnson Guidelines. The calculation for general probate assets remains the same (with $2,500 as the commission calculated for these assets). However, for joint accounts, the Johnson Guidelines provide that a 1% rate is used, regardless of the asset’s value.

So, if A were to die with a joint bank account with a balance of $500,000, we would apply the 1% rate not to the total account value, but to A’s ownership percentage of the account. For example, if A and B were joint owners on a bank account and each held 50% of the account, then only A’s $250,000 would be included in the commission calculation. In this case, we would take 1% of A’s $250,000 in the joint account and arrive at $2,500 for the commission from the joint account. This, plus the $2,500 from probate assets, would result in a commission of $5,000 for this estate.

Other factors to consider when taking an Executor commission

Calculating the commission under the Guidelines is only one step, and the Executor will likely have other factors to consider when it comes to when to take the commission and if they should take the full amount. For more information on this topic, please see our blog post here.

If you have questions about this or other matters related to our practice areas, please click the Contact Us button to get in touch. We’ll be happy to speak with you.

Author:

Stephanie M. Creech

Attorney at Law

Commons & Commons LLP

Experience:

Estate Planning

Estate Administration

Tax matters